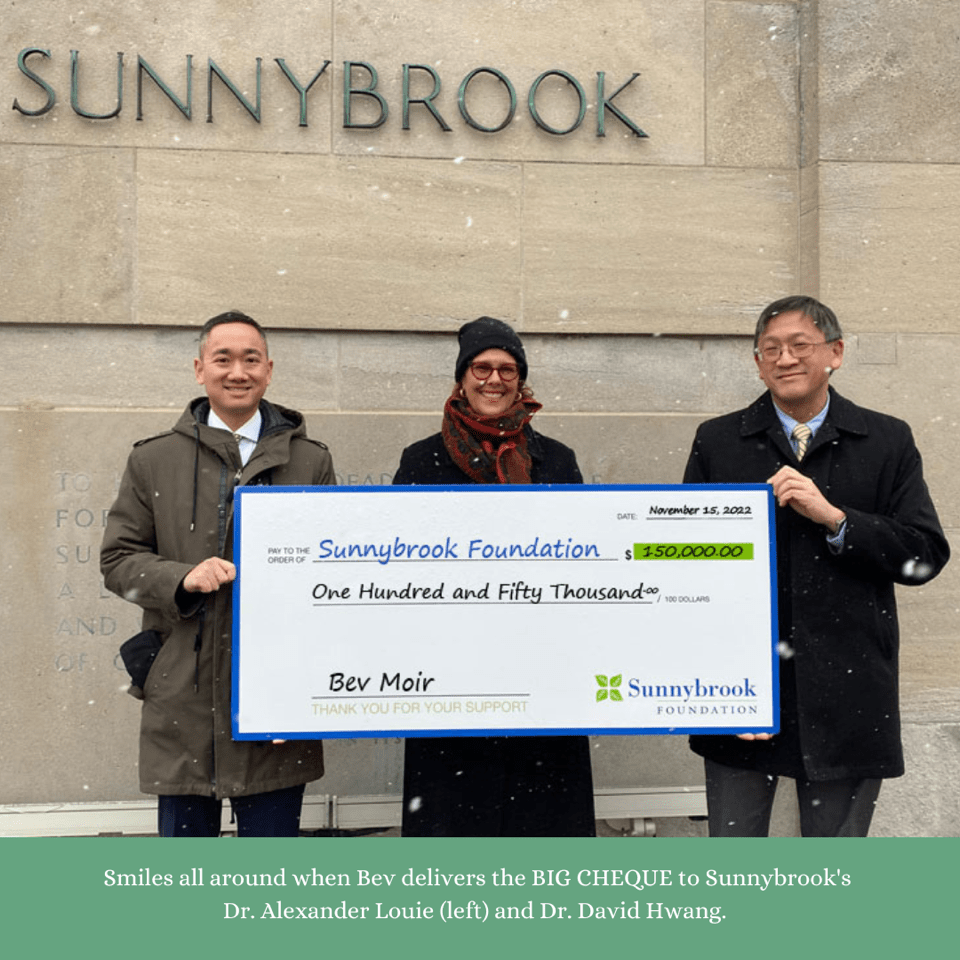

The tally grows with your support!

I’m a glass-half-full kind of person. This attitude is handy when facing cancer and trying to stay positive. So, you can imagine how thrilled I am with hitting close to $500,000 for Sunnybrook Lung Cancer. That means we’re halfway there to our fundraising goal of $1million… an incredible feat in just four years, and I […]

The tally grows with your support! Read More »